Florida Prepaid vs. 529 Savings Plan : Find High Yield through a Historical Analysis

Why Compare the 529 Against the Florida Prepaid Plan?

Parents who want their kids to go to College also want to plan ahead and not be surprised by the cost of tuition of when they turn 18. Thankfully, the State of Florida offers multiple vehicles to prepare for College. Let’s compare the two most popular ones: Florida Prepaid vs. 529 Plans. We will not spend a lot of time explaining the differences between the two plans, but will rather look at them from an investor’s perspective. Many people wonder, is the prepaid plan a ripoff? Is the 529 plan worse than the Florida prepaid plan since it is offered in every state? Here we will look at the numbers and make a determination.

Pros and Cons

Let’s start with some basic pros and cons to set the stage.

| Pros | Cons | |

| Florida Prepaid | -Offers stability -Guaranteed future Florida tuition coverage | -Limited use plan (tuition only) -Not a money-multiplier |

| 529 Plan | -Wide variety of uses (tuition, housing, vehicles) -Can be a money-multiplier | -Can result in financial loss -Does not guarantee Florida Tuition coverage |

Assumptions

In the next four scenarios, we will compare the 529 Plan vs. the Florida prepaid plan in 4 time periods. In order to create a simple comparison, we made the following Assumptions :

- The 529 plan will be represented by Vanguard’s 529 Plan, assuming it is 100% invested in VFINX, a fund which represents the S&P 500. This fund was chosen for its longevity and existence during the time periods we selected.

- Source for VFINX Performance : https://finance.yahoo.com/quote/vfinx/performance/

- The prepaid plan assumes a lump sum payment towards the 4-year university option.

- The prepaid plan cost is represented by the 4-year cost of University of Florida tuition 10 or 15 years in the future.

These are not 100% accurate prepaid plan costs. The historical data on these costs is not readily available- Sources for UF Tuition :

- https://www.collegetuitioncompare.com/trends/university-of-florida/cost-of-attendance/

- http://floridacollegeaccess.org/wp-content/uploads/2013/08/SUS-Tuition-2013-14-Table2.pdf

- Sources for UF Tuition :

Looking at Florida Prepaid vs. 529 over the Past 10 years, The 529 Plan Dominates

Looking back in the 10 years prior to 2020, a 529 plan investment in the VFINX S&P 500 fund would have doubled. This is due to great stock market growth in the past decade. Meanwhile, UF tuition only went up by 11%. If you had the option to make a lump-sum investment in either a 529 or the Florida prepaid 10 years before your child went to college, the 529 would have been the clear winner here. This lump sum investment would have occurred when your child was 8 years old (assuming they go to college at age 18).

Initial Investment : $21,431

| VFINX Capital Gains | VFINX Capital Gains % | UF 4 Year Tuition Difference | UF 4 Year Tuition Difference % |

| $44,164 | 206.08% | $2,174 | 11.29% |

However, A 10-year Window Ending in 2009 Would have Favored the Florida Prepaid Plan

Now let’s look at a less-glamorous 10 years of the stock market : the period resulting in the great recession from the US housing market collapse. We picked this window to represent the worst stock market performance in recent history.

If you had a lump-sum investment in a 529 plan in 2000 for your 8 year child, you would have lost 28% of that investment by the time they went to college. You would have been better off taking the safer option, the Florida Prepaid plan. This is a good example of the 529 plan being a risky vehicle compared to the Florida Prepaid plan.

Initial Investment : $17,491

| VFINX Capital Gains | VFINX Capital Gains % | UF 4 Year Tuition Difference | UF 4 Year Tuition Difference % |

| -$5,024 | -28.72% | $8,708 | 199.15% |

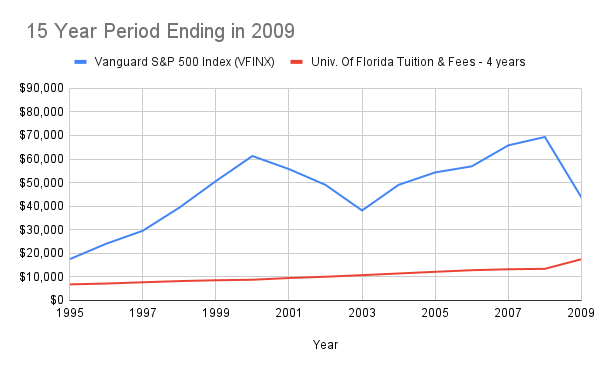

But by Investing 5 years earlier in the 529 plan ending in 2009, You would not have lost your investment

Now here is an interesting fact : if you had invested in a 529 plan for that same child 5 years earlier, you would have grown your investment. It would not have outpaced the increase of UF tuition, but it would still be a positive investment.

You would have still seen the terrible stock market losses of 2008 and 2009, but due to the larger investment window of 15 years, you would have benefited from strong VFINX performance from 1995-2000.

So the lesson learned here is you can mitigate the risk of a 529 plan by widening the time window. You have 18 years until your child goes to college. If you can invest the 529 lump sum in the first 3 years of his/her life, then your investment will have 15 years to grow and weather the ups and downs of the stock market.

Initial Investment : $17,491

| VFINX Capital Gains | VFINX Capital Gains % | UF 4 Year Tuition Difference | UF 4 Year Tuition Difference % |

| $26,182 | 149.69% | $10,672 | 256.48% |

Lastly, if we invest 5 years earlier from the first graph, the 529 plan dominates Florida Prepaid Even More

Now let’s take the same principle of widening the time window, and apply it to our first example – a child going to college in 2020. The gains are massive! By having 15 years to grow, your 529 investment has increased by additional 40%. This shows the strength of a 529 plan during periods of a strong market.

You will also notice that the cost of UF tuition increased by 167% over this period. While this is an alarming increase (something that may scare you into going with the prepaid option) you can see that the stock market still outperformed it at 241% gains.

Initial Investment : $21,431

| VFINX Capital Gains | VFINX Capital Gains % | UF 4 Year Tuition Difference | UF 4 Year Tuition Difference % |

| $51,750 | 241.47% | $8,599 | 167.02% |

Why I prefer the 529 plan over the Florida Prepaid

The 529 plan has a bigger upside than the Florida Prepaid plan. It is a potentially more rewarding plan that is accompanied by a larger risk. Just like any other investment, it is subject to the highs and lows of stock market swings.

The Florida prepaid plan is already factoring in what they believe the costs will be in the future (rather than paying todays rates). It is unlikely that you are getting an amazing deal. When this program first started in the 90’s, you paid todays rates and went to school ‘for free’ once you got there. Not anymore. The program now tries to figure out what the rates will be in the future and have you pay that instead. The prices could go higher than what the plan admins calculate, but being locked in likely isn’t worth it for that risk.

In general, the advantage of a 529 plan is that the investment gains can compound over time. Enjoy your tax-free investment and start a 529 plan early!

This comes down to a judgement call at the end of the day. You will have to determine your level of risk and comfort with the stock market. If you are not looking to grow an investment, stick with the Florida Prepaid plan and treat it like a security blanket. However, if you are hoping to grow your tax-sheltered education investment, go with the 529.

0 Comments